Donned as “Woodstock for Capitalism”, Berkshire Hathaway’s annual shareholder’s meeting attracts tens of thousands of value investors from around the world. Contrarian to the Boglehead’s philosophy, value investors select individual stocks that are traded below their long term intrinsic values. Some of the most notable value investors include the author of The Intelligent Investor, Benjamin Graham, and his student, the Oracle of Omaha, Warren Buffett.

As a Boglehead, I’m all about simplifying and automating, utilizing passively managed index funds and optimizing taxes. So what does a Boglehead think about value investing? On May 3rd and May 4th in University of Nebraska at Omaha’s Mammel Hall, I attended the the 15th Annual Value Investor Conference. Listening to CEOs, authors of best-selling books, investment professionals, university professors, and board members, I tried to soak in as much as I could to apply to my current investment philosophy.

CEO of Morningstar – Kunal Kapoor

CEO of Morningstar – Kunal Kapoor

What were the key takeaways from the conference, and also, Berkshire Hathaway’s annual shareholder meeting?

15th Annual Value Investing Conference

The first non family member CEO of Morningstar, Kunal Kapoor, shared how technology is changing the way companies are being rated by Morningstar. Through machine learning algorithms and the continuous training of these models, stocks can be automatically rated, whereas previously they would have to be manually updated. He did share a disclaimer: these models try and reflect what fund managers believe are important. Bogleheads will quickly rebut with the infamous “Blindfolded Monkey Beats Humans With Stock Picks“. Who knows if the fund managers are right?

It’s apparent that non-technical individuals, albeit being potential “geniuses” in another sub-culture, may not completely understand the nuances, complexity, and unpredictability involved in, say, technology companies. Coupled with a shrinking product life cycle, it’s hard to predict how a company will do in the future. Even Warren Buffett strays away from technology companies. He only invested in Apple because he views Apple as a Luxury Consumer Products company, not a tech company. As he has told CNBC, “Apple strikes me as having quite a sticky product and an enormously useful product to people that use it, not that I do”.

Author of numerous corporate finance books and The Deals of Warren Buffett, Glen Arnold shares some of his thoughts with the conference attendees. He notes that Buffett learns as much, if not more from his mistakes as from his successes. The most important thing is to minimize a fatal error when possible, based on the most recent up-to-date information. Again, hindsight is 20/20. However, all we can do is accept error as part of the investment process, and learn and grow from past mistakes.

Founder of Giverny Capital, François Rochon, had one of the more interesting presentations. He viewed value investing as an art form, where original and creative minds tend to find more success than conventional investors. He differentiates between the two in five categories:

The Evergreen path, presented by Founder of Tugboat Ventures, Dave Whorton, proposed a paradigm many can get behind. He looks for businesses with high character CEOs and quality managers, not unlike what Warren Buffett does. The business must start with a purpose greater than money. An engaged and loyal workforce, coupled with longer planning horizons, were praised by Whorton as significant competitive advantages in today’s economy. The 7Ps he proposed included: purpose, perseverance, people first, private, profit, paced growth, and pragmatic innovation. However, as non-institutional investors playing with money mostly in the four to six digit range, how can we know what’s actually going on behind closed doors?

The last presentation I want to cover was done by Guy Spier, who tried to find the true source of competitive advantage in an overpriced world. His ideals resonated with me, as it seems that we both are fascinated by organizational behavior, specifically giving more than we take to create a culture of success. In a world where everything was wiped out, but your social status, he poses a question: would I (Guy) or Warren Buffett have an easier time starting a successful venture? He opens up with an anecdote about how he bid $650,100 in 2007 for a charity lunch with Warren Buffett. Despite Warren’s perceived tightness, he was always giving; Warren ended up giving hundreds of dollars as a tip to the waiters, a genuine gesture of appreciation for their services during lunch. From that waiter’s perspective, Buffett has made a lasting impression, which could be described as “social goodwill”.

This is what Guy wanted to drive home; giving more, not necessarily only in monetary value, can help better the world, not to mention be extremely fulfilling. This goes hand in hand with “The Most Useful Skill in the World” where I covered “nachas”, a Yiddish word for “pride and satisfaction that is derived from someone else’s accomplishment”. Influenced by my favorite organizational behavior author, Adam Grant, Guy depicts a similar world, where giving to others will accrue invaluable goodwill.

The Annual Shareholders Meeting

Here are a few key takeaways I thought were interesting from the actual shareholder’s meeting:

- Roughly 10% of assets are managed by Ted Weschler and Todd Combs, whereas Buffett and Munger oversee the other $300bn

- The goal of healthcare is for Berkshire and all affiliated with Berkshire to gain access to quality healthcare–the main goal is not profit

- Berkshire wants to be (perhaps is) the preferred buyer of companies. Why? They don’t mess with the culture! If Berkshire has selected a company already, the board of directors and management down to the balance sheet are already “on point” per Warren Buffett

- Berkshire is sticking with Wells Fargo – Buffett doesn’t know who was responsible for the scandal, but he emphasized how the vast majority of employees are innocent, and that only a select few should be punished

- Dividend is unlikely, but share buyback would be more likely to use some of the $116 billion cash hoard

Thoughts…

From a holistic viewpoint, value investing sounds much better than the vast majority of investing philosophies. I do have a few qualms with this, however. From talking with experienced fund managers who are self proclaimed “value investors”, they prefer a portfolio of roughly 30-40 stocks or mutual funds/ETFs, enough diversification in case one or two bad eggs slipped through. However, from spending time researching the companies to stressing about keeping up with the companies, that energy could have been diverted into something more meaningful: family, friends, new skills, etc. For many, researching companies is a legitimate hobby, passion, or job, thus I say keep on keeping on! However, for the layperson who is not that interested in investing, or for someone who simply does not have the time, perhaps a lazy portfolio or even a target date fund (see below) will suffice. If most fund managers and individual investors do not outperform the S&P 500, perhaps it’s time to swallow your pride and index it up!

Buffett spent the first 15 minutes of the shareholders meeting–right after the introduction video–blessing index funds, specifically the S&P 500. However, what I believe is that we should bet on the whole market, or at least a large portion of the market. Through Total Stock Market Indexes (U.S. and International), we can touch a decent portion of the world’s largest businesses. Obviously, there will be dogs, but as long as the economy on a macro level does well, these funds should also do well. To read up on the case between Total Stock Market Indexes vs. the S&P 500, check this article out featuring John Bogle, founder of Vanguard.

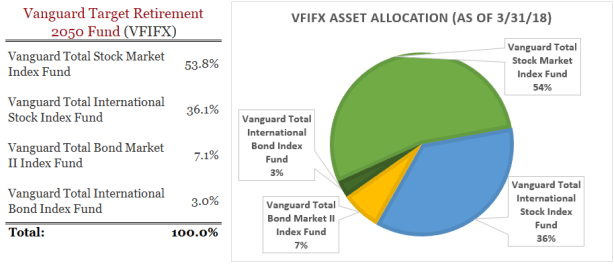

Here is a snapshot of Vanguard’s Target Retirement 2050 Fund (VFIFX):

Vanguard’s 2050 Target Date Retirement Fund Asset Allocation (VFIFX), 15bps fee

Vanguard’s 2050 Target Date Retirement Fund Asset Allocation (VFIFX), 15bps fee

Although I’m a fan of index funds or target retirement date funds (for simplicity and more diversification), there were some ideas that I really enjoyed listening about and learning, which are listed below:

Too Long, Didn’t Read…

- Technology (Machine Learning & AI) are helping automate ratings on Morningstar

- Warren Buffett views Apple not as a tech company, which led to him investing in it (multiple times)

- Minimize fatal errors when choosing a company to back (buy their stock) – be open minded and learn from your errors

- Be “unconventional” for unconventional returns; focus on the long term, choosing what to OWN, while maintaining an agnostic/open mindset

- Choose businesses with quality leadership focused on the long term, an engaged workforce, and one that’s powered by a purpose greater than money

- Although contrarian, try to give more than you take to build social goodwill 🙂

- Berkshire Hathaway has developed a succession plan and has been engaging in “little bets” for the next generation of leaders

- More Apple, confident in Wells Fargo, likes healthcare not as profit center, but to give employees better benefits

- Berkshire wants to be the preferred long term partner with companies

- We shouldn’t throw the baby out with the bathwater (keep an open mind/agnostic viewpoint on a lot of things)

Picture with my cousin in front of the meeting arena (Century Link Center)