For over twenty years, credit scores have impacted us in virtually all of our major life decisions. With over 10 billion FICO® scores accessed by creditors in 2013, it’s safe to say that we now live in an era where financing is the norm, and how likely you are to pay on time has been boiled down into an algorithm that is your credit score.

In attempts to increase transparency and in exchange for your personal information, banks such as Chase and personal finance software services such as Mint now display what factors make up the credit score. Because there are so many different types of credit scores, depending on the industry, scores may vary. Mint gives the TransUnion VantageScore, which is a model created by the three major credit bureaus (Equifax, Experian, and TransUnion) designed to compete against FICO® whereas American Express uses FICO® Score 8 based on Experian data.

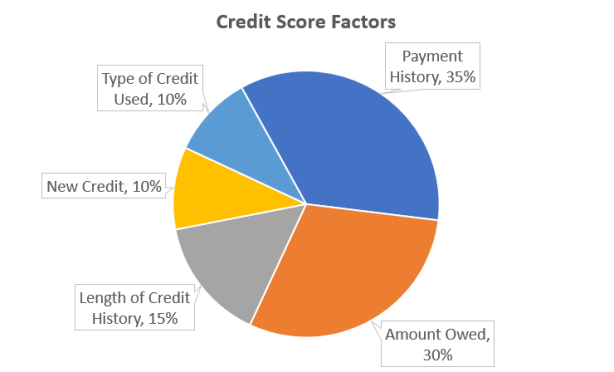

Although the FICO® scoring algorithm is proprietary, we can estimate what categories affect the score the most. The scoring system (generally) has five major factors:

Source: https://blog.myfico.com/5-factors-determine-fico-score/

Plugging these five factors into the algorithm, a number ranging from 300-850 gets outputted. This is the credit score. According to Experian, having a credit score of 670+ is considered “good”:

According to Experian, only 8% of debtors within the 670-739 range are likely to become seriously delinquent.

Let’s explore how a good credit score can help us! When we apply for auto credit, creditors grab our “FICO® Auto Industry Option” score, only available to car dealers and finance companies. The auto scores care more about how we’ve managed our previous auto loans. It looks at if you’ve ever had late payments on a current/previous auto loan or lease, settled an auto loan or lease for less than you owed, had a car repossessed, had an auto account sent to collections, or if you’ve included a car loan or lease in your bankruptcy.

A dirty trick that some car dealerships play is that they pull both your traditional FICO® scores and your FICO® auto scores. The scores will vary, and they will try and increase their profits by showing you your lowest scores, thus increasing the interest rate they charge. [1]

Interest rates tend to be inversely related to your credit score; as your credit score goes down, your interest rate goes up. Here’s an example using a $24,000 Honda Accord:

Even though the car price, payment term, and the down-payment amount are all the same, person B will end up paying $7,513.55 MORE than person A! Having a large interest rate can force us to pay more for the same thing!

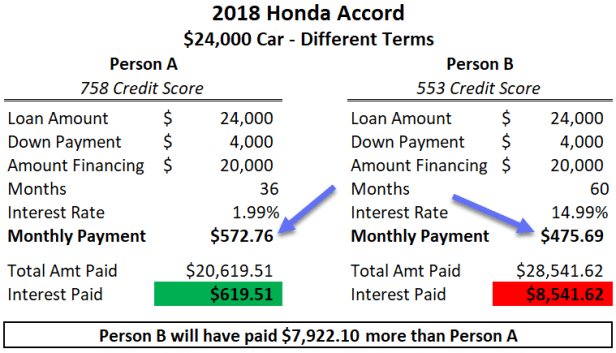

Another trick to avoid at the dealership is to not focus on the monthly payment, but rather the purchase price. Take a look below:

Even though person A pays almost $100 more than person B, person B will have paid $7,922.10 more than person A when everything’s paid off! Generally speaking, no more than 10% of your gross income should be going to car payments and insurance a year. However, monthly payments (thus annual payments) can be extremely misleading!

To optimize your car-buying experience, call your dealership ahead of time and ask for what credit reporting agency their lenders use, what type of FICO® score they use (regular/auto), and what other factors other than credit scores go into their decision-making process. Furthermore, try to get pre-approved by your bank or a credit union to get more competitive rates.

Credit has revolutionized how the modern world handles transactions. Just as money has replaced bartering, credit, in the form of credit cards and loan information stored digitally, will replace hard money/currency. Conceptually, going cash-less has limitless benefits, but when actually implemented, educating the masses on credit and how to use credit responsibly to avoid being over-leveraged arise as obstacles to overcome.

[1] https://ficoforums.myfico.com/t5/Auto-Loans/FICO-Auto-Enhanced-Scores/m-p/228198

Great tips! I found this over the web a few moments ago, this may help others as well on how they can improve their credit score https://www.htpenterprisesfinancial.com/5-great-ways-to-improve-your-credit-score-htp-enterprises-financial/ feel free to click the link

LikeLike