Why are we taught to save 10%-15% of our income? Where does this number come from?

First, let’s determine what is the most important driver of retiring wealthy. Is it income? Is it choosing the right investments? Nope. It’s the almighty savings rate.

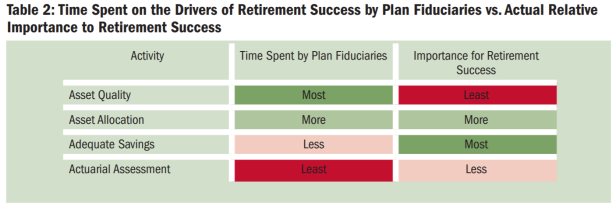

In the Summer 2011: Volume 41 No. 3 Journal by American Society of Pension Professionals & Actuaries (ASPPA), the most important driver for retirement success is the savings rate, detailed as “Adequate Savings”.

The ASPPA Journal, Summer 2011: Volume 41 No. 3

The ASPPA Journal, Summer 2011: Volume 41 No. 3

Now that we know how important the savings rate is, what exactly is the savings rate and why does everyone and their mother tell us to save 10%-15% of our income? Where does that number even come from?

The savings rate is calculated by:

[ ( Take Home Pay – Spending ) / (Take Home Pay) ] x 100 = ____ % Savings Rate

Let’s take a person taking home $40,000 a year and spending $36,000 a year:

[ ( $40,000 – $36,000 ) / ($40,000) ] x 100 = 10% Savings Rate

Not too bad!

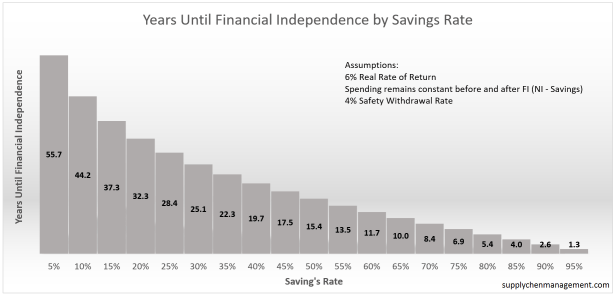

Let’s take a quick look at how many years it will take to retire, starting at $0, at different levels of savings rates:

Assuming a 6% annual real rate of return, spending remaining constant in retirement from the working years, and a 4% safety withdrawal rate (SWR), we can see that it will take roughly 44 years to retire at a 10% savings rate and roughly 37 years to retire at a 15% savings rate.

A Safety Withdrawal Rate is defined as the quantity of money, expressed as a percentage of the initial investment, which can be withdrawn per year for a given quantity of time, including adjustments for inflation, and not lead to portfolio failure.

*Where failure is defined as a 95% chance of success (portfolio not running out)

Now, I labeled this chart as “Years Until Financial Independence” because many people choose to keep on working after they reach financial independence. Financial independence merely gives options financially dependent people cannot afford.

A 4% SWR has a >98% success rate, tested by the Trinity Study conducted by Phillip L. Cooley et al.

Let’s take a young college graduate at the tender age of 22. The young graduate enters the workforce and starts allocating 10% towards retirement and consistently does so every year without fail. Because it will take 44.2 years to achieve financial independence at a 10% savings rate, the young professional will be able to retire at (22 + 44.2) = 66.2 years old. At age 66, American citizens are considered “fully retired” according to the SSA (Social Security Administration).

What happens at 15%? 22 + 37.3 = 59.3 years old. In 2016-17, the IRS allows contributors to start withdrawing from their retirement accounts at age 59 1/2. Interesting how a 15% savings rate will meet that target for a fresh college graduate that consistently saves that much a year.

No wonder we’re told to save 10%-15% of our income!

We’ve touched on the rigid recommendations incessantly repeated by financial planners and elders, but what happens if we think outside of the box and engage in aggressive saving?

As we increase savings, at a 4% SWR, we can achieve financial independence in 32 years with a 20% savings rate and with a 65% savings rate, we can retire in 10 years! This, of course, is subject to change depending on life events and changes such as mortgages, children, health issues, etc.

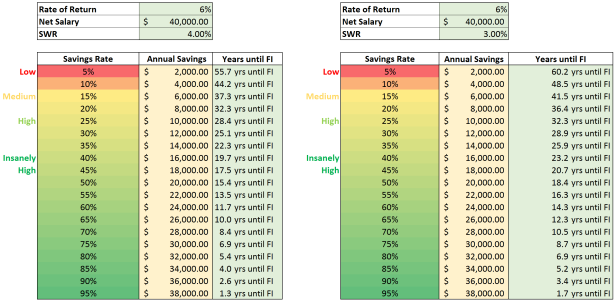

On the left, we see a safety withdrawal rate of 4%, used in the bar chart above. To eliminate the slim chance of the portfolio running out, we can use a 3% safety withdrawal rate, where according to The Trinity Study mentioned above, returns a 100% chance of the portfolio never running out, regardless of asset allocation. Keep in mind that the Trinity Study is quite old; nothing is guaranteed but we can reduce the likelihood of the portfolio drying up.

It’s crucial to note that the annual savings is tied to the net annual salary (take home).

Annual Savings = Net Annual Salary – Annual Spending

This is perhaps the most important concept. Your salary does not necessarily dictate how well off you will be in retirement. The more you save, the less you spend. The less you spend, the less you need in retirement!

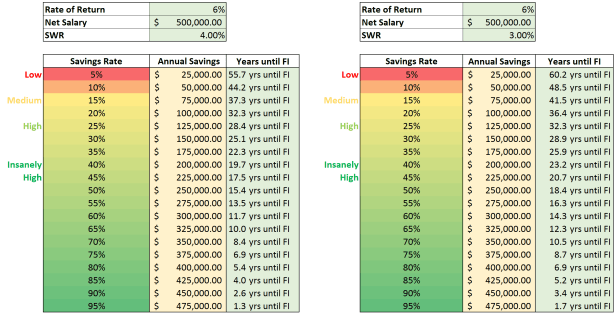

Let’s take a gander at someone making $500k:

NOTICE HOW THE YEARS UNTIL FINANCIAL INDEPENDENCE (FI) DON’T CHANGE! This is because even though they’re saving so much, they’re SPENDING so much more, thus they need MORE in retirement to sustain the life they’ve built up.

To combat “keeping up with the Joneses” but also not deprive oneself on the journey towards financial independence, balance must be achieved. In other words, “Build the life you want, then save for it”. To figure out how much is needed to achieve financial independence, multiply your annual spending by 25x (4% SWR) or 33x (3% SWR) to find your goal. Once you’ve found your goal, tinker with Supply Chen Management’s Nest Egg Simulation Calculator to see if you’re on track.

Now we know why we’ve been told 10%-15% is the magic percentage to save: 10% a year will allow a college graduate will retire the same year as SSA’s definition of “full retirement” and 15% a year will allow a college graduate to retire right on time to tap into retirement accounts without penalty! The almighty savings rate, overlooked by most because of its boring and derivative nature, and revered by those who know its true value.

Does a 10%-15% savings rate make sense for you? If not, what is your savings rate? Comment below!

Dear Wayne,

You have done a great job to show that how small saving will change our life with very detailed data and charts.

Keep doing the good work and you will reach your gold sometime soon.

My invitation for you to attend Berkshire Hathaway annual shareholder meeting to meet Warren Buffett and other greatest investors in the World is always extended.

Dream big and work hard.

Loved

Uncle John

LikeLiked by 1 person

How do you account for pretax savings (like 401k) into your savings rate formula?

LikeLiked by 1 person

Hi Rich,

Thank you for the great question. This was something I wasn’t sure whether to include or not. In the end, I decided that adding a layer of complexity with pre/post tax savings did not mean much when trying to communicate how we can break the “traditional paradigm” of retirement.

For this reason, I have lumped all savings, regardless of if they’re pre or post tax, into one bucket for simplicity. Ideally, we want to diversify the buckets in which we hold our investments, giving us more options to optimize our tax obligations up front and in the future (at least with current knowledge). The types of vehicles we choose could potentially artificially under or overstate our current savings rate and thus alter our calculated time to retirement.

LikeLike

I believe a 10%-15% savings rate is the bare minimum. Preferably I’d like to see maybe 20%, or even more if one has no debt!

LikeLike

I completely agree! Something I’ve been personally struggling with is achieving a healthy balance between saving for the future and spending on the present. I guess that will vary from person to person.

LikeLike

You actually make it seem so easy together with your presentation however I find this matter to be actually something which I think I might never understand. It seems too complex and extremely huge for me. I’m having a look ahead for your subsequent post, I’ll try to get the cling of it!

LikeLike

Wow, amazing blog layout! How lengthy have you been running a blog for? you made running a blog look easy. The total look of your web site is wonderful, as smartly as the content material!

LikeLike

Hi Alex,

Thank you for your kind words. It’s been a little over a year now since I started the blog. When building wealth (nest egg for retirement or on the path to FI), the important thing to remember is to increase your income, decrease your expenses, and invest the rest!

LikeLike