What truly matters?

What matters to one person may not matter to another person. As humans, we normally equate our time with money, where money can buy time. In other words, we can spend money for goods and services we would otherwise spend time and energy to create.

I can purchase a sandwich from a deli for lunch, or harvest my own wheat and separate the wheat from the chaff for flour, extract salt from the earth for flavor, collect fresh water, etc. And that’s only for the bread! What about creating the fire and oven for baking, or tools for measuring and carrying water? Thus, we all assign a value to anything we spend money on; if the perceived utility (benefit) exceeds the costs (cash, time, energy), then that transaction will likely manifest into reality.

A lot of people choose to focus on budgeting; brew your own coffee and save $5 a day, invest it, and you’ll eventually become a millionaire! Does the math add up? Not quite if you compute the numbers conservatively, but perhaps the utility from that cup of coffee exceeds the $2,000 a year price tag.

Now, $2,000 invested every year for 40 years will yield roughly $300,000 in today’s dollars, using Supply Chen’s Nest Egg Calculator. This is quite an impressive nest egg just from forgoing coffee.

Sounds simple enough. However, are we tricking ourselves into thinking we’re financially savvy?

Do any of the following scenarios sound familiar? I have…

- chosen a $18 entree that looked “good enough” instead of a $22 entree, when the $22 entree was the one I really wanted

- chosen the store brand soda for a celebration party I was hosting to save a dollar

- chosen against “supersizing” a meal purely because of financial reasons ($2)

- chosen to wake up my spouse at 3:30 am to drive me to the airport instead of spending $30 on an Uber, and I knew that would pose a huge inconvenience to him/her

- turned 2-ply toilet tissue into two 1-ply rolls

I know I’m definitely guilty of some of the above. Now, I’m not suggesting to splurge on thousands of small purchases a year, but rather to spend more time on the large piece of steak on your plate instead of the peas. [1]

The Pareto Principle

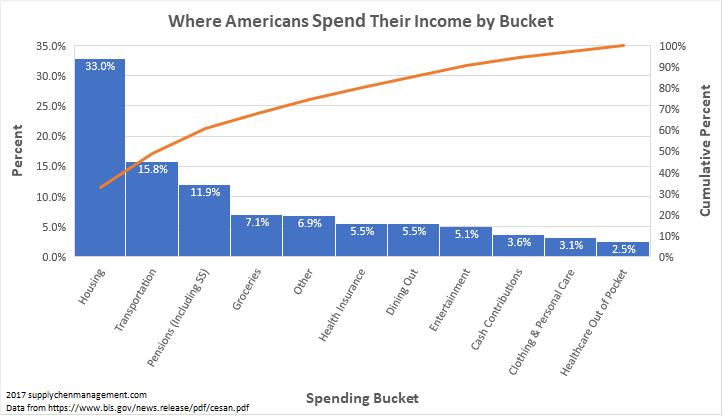

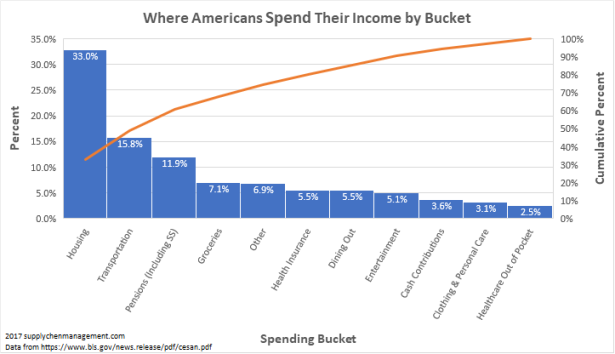

Enter The Pareto Principle, otherwise known as the 80/20 rule. It advises to focus on the 20% of causes (actions) that will generate 80% of the effects (results). Even though the ratio will vary, the ideology stays the same: focus on the few things that will generate the big wins. There are two sides to the equation: Income and Expenses. According to the 2016 Consumer Expenditure data from the Bureau of Labor Statistics, average expenditures were $57,311 per unit. [2]

Here is the expenditure breakdown in a Pareto Chart format:

The orange line shows that over half of the result is dictated by the first two buckets: housing and transportation. It seems that the average American (surveyed here) spent roughly 5.5% of their income on dining out. Is this something to focus on? Perhaps, if you’ve done everything possible to achieve your “big wins”.

What are some big wins?

Five HUGE Wins

- Automate Your Finances – If you don’t see it, you can’t spend it.

- Automate extra payments towards higher interest debt

- Automate money to your savings account

- Automate 401k and IRA contributions

- Set it and forget it 🙂

- Optimize Big Ticket Expenses – Identify your largest spend buckets, most likely housing, transportation, & taxes, and focus on reducing these.

- Housing – Could you get a roommate? Does it make sense to live in a smaller space?

- Transportation – Do you really need a luxury vehicle? What utility would a brand new car bring you?

- Taxes – Could you reduce your taxes through contributing to a traditional retirement account? Could you engage in tax loss harvesting?

- Increase Your Income – Find a job with good pay & benefits

- A $5,500 salary bump in your mid-twenties, consistently invested in index funds over 40 years, will amount to close to $1 million by age 65!

- Invest in Yourself – If you’re not learning, you’re not growing.

- Read books

- Take MOOCs or pursue certifications

- Challenge yourself; adapt and be agile

- Adopt a mindset of “speak as if you’re right, but listen as if you’re wrong” [3]

- Quit Procrastinating – Borrowing the slogan from Nike… JUST DO IT.

On the flip side… We must brainstorm what our “Big Losses” are, and how we can avoid them to mitigate risks.

Don’t Be Cheap; Be Frugal

Cheap is when you cut costs for the sake of cutting costs. Frugal is when you take a step back and look at the big picture and maximize value. In the show “Extreme Cheapskates”, Roy chooses to reuse paper towels, boasting that he’s saved an estimated $2,000 over the past 10 years.

Thankfully, he’s not hurting anyone else by choosing to do so. However, another example could be ordering the most expensive item on the menu, but giving a small tip. The person on the other side most likely depends on tips to live, as the minimum tipped wage for many states fall way below these states’ minimum wage. Perhaps skimping on tips may not be the most socially responsible; this action definitely screams “cheap” and not “frugal”.

By choosing what you value, you can have more of what you want. In the wise words of Paula Pant, “You can afford anything, but not everything”.

[1] https://youtu.be/a1bJ-spR8Sg

[2] https://www.bls.gov/news.release/pdf/cesan.pdf

[3] Adopted from Karl Weick, Rensis Likert Distinguished University Professor of Organizational Behavior at the University of Michigan

I’ve never heard of MOOCs (massive open online course) – I’ll have to check them out.

I also used to be guilty of buying the cheapest toilet paper. Every time I bought some, I’d immediately regret it and tell myself that I wasn’t going to be so cheap next time. The problem was that I would buy in bulk, so by the time I needed to buy toilet paper again, I’d forget what I bought before, and I didn’t want to buy the most luxurious and expensive brand… So I ended up being back where I started!

LikeLiked by 1 person

I love this article! As an Uber driver, I make sure I tip all my service workers nicely. Also, nice use of Paula Pant’s Afford Anything, But not Everything mantra! Her show is awesome

LikeLiked by 1 person

MOOCs are amazing! My favorite platform is EdX. I love how such reputable higher learning institutions are giving learners access to quality education, at little or no cost. I am a fervent believer in sharing information to better society; the pie can and should be expanded.

Your toilet paper anecdote made me laugh. I’m sure your bum has been thanking you every day since the switch!

LikeLike